Not all opportunities are the same: A look at the four types of entrepreneurial opportunity

Opportunity is firmly implanted within the entrepreneur’s mind and vision

All human activity is directed at some perceived possible future. Our life is dominated by the channeling of our efforts towards creating the future we anticipate for ourselves. The future is a journey for which we are not certain, relying upon our imagination to picture what this future would be like, whether it is just in five minutes or five years time. We can only be certain about this future when we get there [1]. The heart of seeing opportunity is about seeing the future, a process that doesn’t occur through formal analysis, forecasting or strategic planning process. Rather, opportunity is about seeing the future for what it could be through our aspirations and imagination in ways that other people don’t see. There is a passionate, visionary, and exciting side to opportunity that formal systems and theory does not capture adequately. Opportunities create a path where various levels of enthusiasm, skill, resources, rigidity and commitment, and a devised strategy are pursued by individuals and firms. This journey begins with the identification of an opportunity upon which we are inspired and motivated enough to pursue, not always knowing where we will end up. Our actions test what we are anticipating, inferring, that pursuing opportunities is about learning.

Opportunity cannot be explained by environmental forces or individual factors alone as they are both very much interrelated[2]. The phenomenon of opportunity spans across the disciplines of micro-economics, psychology and cognitive science, strategic management, resource based and contingency theories that are patched together, synchronized and added to form new information in the form of ideas. Opportunity is a situational phenomenon that is developed from incomplete information [3]. Opportunity relies on an individual recognizing, discovering or constructing patterns and concepts that can be formed into ideas. Opportunity is a poorly defined concept where theories are good at explaining creation after the event, but been very poor in predicting creation. Theories are limited in their explanations and can only point to what capabilities exist when the individual is developing opportunities. Opportunity models that have been developed by strategy and marketing researchers have difficulty in being applied to entrepreneurial start-ups. Pre-1970s it would have been totally inconceivable to predict that a group of young entrepreneurs who dropped out of university were able to move into the computer industry and be so successful exploiting opportunities that incumbent Fortune 500 firms like IBM couldn’t [4].

The central aspect of opportunity is being able to see it in the first place and acting upon it before others. This is a function of how we perceive the world and process information. The resulting intuition, vision, insight, discovery, or creation is an idea which may upon evaluation become an opportunity. This ability is not uniformly distributed throughout the community[5], as people have different orientations towards time and space.. Thus the opportunity gestalt is not a uniform or regular phenomenon that any theory can provide a general explanation[6].

Opportunity is a dynamic construct that ebbs and flows according to a continually changing environment. This also occurs in what were once called traditionally “stable industries” like broadcasting, entertainment, chemicals, pharmaceuticals, automotive, and aviation. Customer trends, resource costs, government regulations, changing trade conditions, competitive products, merging industries, and other types of pressures and shocks like rising petroleum prices continuously shift the panorama of the environment and thus change is the prime generator of opportunity. The financial crisis of 2008 coupled with international monetary shifts, changing exchange rates and the movement of manufacturing and jobs from Western countries to China are phenomena that change national economies and the balance of world markets, bringing massive structural shifts and potential opportunities. As we saw in 2008 this process can be extremely rapid and appear to occur with little warning just like the ‘peoples’ revolutions’ in Tunisia, Egypt, Jordan, Yemen, Bahrain, and Libya during 2011. One of the many effects of these changes has been the dramatic shift of firms to manufacture in China.

Over the last forty years we have witnessed the creation of many new multi-billion dollar industries like modern biotechnology, discount retail, mutual funds, cellular telephones, personal computers, satellite television, and the internet. Industries that were important to the growth of the US during the larger part of the twentieth century like steel have massively declined, leading to the demise of giant Fortune 500 companies like Bethlehem Steel. Companies like Intel, National Semiconductor, Microsoft, Apple, Nokia, Amazon, eBay, and Wal-Mart have risen to dominance in their industries, each in their own way transforming the way a particular industry works. The changeover of industry dominance has been so rapid that 40% of the Fortune 500 companies that existed in 1975 were no longer operational two decades later [7]. Today 33% of the most successful firms’ profits are generated from products launched within the last five years [8]. In some industries like the mobile phone, television manufacture, white goods and automobiles, etc this figure is much closer to 100%.

Firms need to continually renewal themselves through taking on new opportunities by developing and launching new products, services and/or creating new business models. Companies need to shift their strategies flexibly as the characteristics of opportunities change and pursue emerging opportunities to remain successful. There however is a tendency for successful firms to become so focused upon the internal processes of their organizations that they forgot to scan the environment and to see where the marketplace is going.

The subjective nature of opportunity makes it impossible to separate the concept from the individual. Opportunity has a deep basis in a person’s prior knowledge and experience, personal aspirations, imagination, and fear of uncertainty. As opportunities are situational, so must be the practice of entrepreneurship and thus it is very difficult to agree on a common definition. What may be entrepreneurial in one context may not be entrepreneurial in another time and place, so entrepreneurship is also a relational concept. As entrepreneurship is also carried out within a social context, entrepreneurship must also be a cultural phenomenon.

Entrepreneurship can be seen as an individual or collective way of thinking, constructing an opportunity attached to a vision, which somehow precipitates the gathering, co-opting, combining and organizing of resources into enactment upon the opportunity with the goal of activating the vision, utilizing knowledge, technology, and business tools in a relatively novel way to realize results, that have the possibility of creating a sustainable organization, where there are willing followers who share the vision. The concept of novelty is also situational, relational, contextual, and cultural, and the standards of novelty – meaning the quality of being new, will be different in say the United States to what is novel in The Ghana, Nepal, Bangladesh, or Fiji.

Most ideas have their basis in some old idea, something seen or experienced within the past, so from this point of view most opportunities are not truly novel. For example, an old type of business can be given a new business model and professionalism like McDonalds did for burgers and Holiday Inn did for motels. New technologies can be applied to old products and processes like desktop publishing and email and domestic business models can be expanded internationally like Coca Cola and Pizza Hut.

Many people mistake their aspirations for opportunity. For example, people put their money and efforts into a boutique, restaurant or spa for the wrong reasons because they like fashion and shopping, food and cooking, or aromatherapy and massage, only to close down a few months later because there was no real opportunity. In SME’s the values of the founder and the firm are the same in many cases. Business opportunity is influenced to various degrees by a hierarchy of personal and family aspirations and concerns that cannot easily be separated from business goals. This can be dangerous if one is unaware of this influence upon thinking.

Our knowledge and personal goals are embedded within our imagination which is at the heart of our existence, a cognitive quality that we would not be human without[9]. Imagination extends our experiences and thoughts, constructing our view of the world to lower our uncertainty of it. Just like imagination is a good way for novelists to create their stories, imagination is needed to create new value sets to consumers that separate new ideas from others. This requires originality to create innovation [10]. Imagination is the essence of marketing opportunity[11] that conquers image and fantasy to consumers, allowing them to imagine what it would be like to live at Sanctuary Cove in Northern Queensland, Australia, receiving a Citibank loan, driving a Mercedes 500 SLK around town, or holidaying in Bali. Imagination aids our practical reasoning [12] and opens up new avenues of thinking, reflecting, organizing the world, or doing things differently. Imagination decomposes what already is, replacing it with what could be, and is the source of all our hope fear, enlightenment, and aspirations.

There are really very few innovators in the business world as most firms tend to adapt, emulate, and follow other proven ideas. By emulating and matching other firm’s ideas and strategies, and adopting the behaviour and actions of others, just like we did in the school playground, we reduce our personal risk and uncertainty. By far the majority of businesses follow others that successfully exploit opportunities, rather than seek their own to exploit.

Each story about a successful (or unsuccessful) entrepreneur is unique and has its own particular reasons for success (or failure) based upon the type of opportunity, skills, focus, apt timing, resource configuration, personal competencies, and a strategy for the situation, which may or may not be right for the particular opportunity and entrepreneur. Different kinds of opportunities will lead to different types of strategy and venture form, which leads to different types of enterprises, business scope, and ways organizations are run. Any individual case studies only show a limited opportunity set, resources, skills, and capabilities, source of opportunity, and strategies for a particular situation. For each and every situation all these factors will be different.

Some companies rapidly grow after start-up because they have correctly identified an opportunity, have the right capabilities, networks and resources, and devised the correct strategies to exploit the opportunity effectively. Other firms may take a longer time to learn the heart of the opportunity and what is required to successfully exploit it, or may be under resourced and need to build their capabilities, so growth is much more modest.

The basis of a new entrepreneurial venture is coming up with something that others don’t have. Breakthrough or revolutionary ideas may take some time for consumer acceptance where the speed of success may depend upon the extent that consumer habits must change, the convenience of the purchase process, and the familiarity with the channels of distribution. Sales revenue will be very difficult to predict, if not impossible and the only confidence an entrepreneur may be able to have in the future outcome is that their new product or service offers substantially more value than what is currently in the market. How quickly the product catches on, is really anybody’s guess [13]. New start-up firms may only be able to fulfil niche segments due to the large costs of blanket market distribution. At the other end of the continuum, products that replicate other competitive products or are only marginally better are difficult to introduce and gain any deep market penetration. These products may compete on price, value (more product for the same price), or other short term market tactics. Success in any competitive environment may just come down to the hard slog of out pacing the other competitors which drains profitability for all concerned.

Strategy is the driver of opportunity exploitation. However, it must be flexible in adapting the idea, objectives, organization, product, strategies and tactics, as they are all paramount for success. Strategy based on opportunity relies on learning, building capabilities, and making venture choices that are based upon our subjective preferences. Performance along the opportunity path will be measured against a person’s own personal vision as a benchmark[14].

Although entrepreneurs come from all walks of life, backgrounds, and ventures are vastly different, there is perhaps a common narrative and shared curiosity that would entail thoughts like ‘why is this so?’ ‘Is there a better way of doing this?’ ‘Is there a way I can benefit?’ and ‘How can I improve upon it?

What is Opportunity

There are a number of definitions of opportunity that provide different glimpses upon its meaning. One of the most relevant definitions to this book was developed by Stevenson and Jarillo who saw opportunity as a future situation that is both desirable and feasible[15]. Wickham saw opportunity as a gap in the market where the potential exists to do something better that creates value[16]. From the Schumpeterian point of view an opportunity is simply a chance to meet a market need through some creative combination of resources to deliver superior value[17] Scott saw opportunity as a recombination of resources that results in new products, services, or changes within the value chain[18]. Stevenson and Gumpert (1985) saw that for an idea to be classified as an opportunity, it must meet two criteria; Firstly the idea must represent a desirable future state involving some form of change, and secondly the individuals involved must believe that it is possible to reach that state[19].

The implications of the above definitions view opportunity as a perspective taken about the possible future state of the environment, a potentiality that is not yet actualized that may or may not be feasible. Opportunity is a juncture where something favourable can be realized through undertaking certain activities to realize the identified potential, based on a set of ideas and beliefs that enable the creation of goods and services that do not yet exist[20]. For example a computer without an operating system is useless to most users and be of very little market potential. But the advent of an operating system adds value to the computer. There are many instances where consumers are not able to articulate their needs and wants for certain new products until they see them and are able to recognize or learn about the value the product or service may have[21]. Opportunities can be exploited by fulfilling these needs, wants, or creating trends and fads with goods or services that offer value to consumers. For example, consumers may not see the need for a toothbrush sterilizer until they see one on the market and are presented with information about the bacteria build up on a toothbrush lying around in the bathroom cabinet. Therefore to see opportunity one must understand the technical aspects of the nature of the opportunity or have an intimate understanding of the value chain involved.

Opportunity implies some form of action to realize the potential, which infers entrepreneurship. It is an entrepreneur who develops an idea from some formation process, develops the goals to pursue the opportunity and has the motivation to assemble resources, and utilize networks and skills in the pursuit of exploitation.

The Global Entrepreneurship Monitor (GEM) makes a distinction between necessity based and opportunity based entrepreneurs. Necessity entrepreneurs take up self-employment out of a need to earn income as the prime motivation, where very few other viable economic alternatives exist. Opportunity entrepreneurs take advantage of perceived business opportunities. Their desire may arise out of dissatisfaction with their current life situation[22] or out of awareness about a growing number of opportunities arising out of economic growth with new optimisms[23] . It is the author’s view that GEM reports have consistently overstated opportunistic entrepreneurship and understated necessity entrepreneurship in developing countries due to interview methodologies and bias as people tend to put their position in the best light during formal interviews. Personal life situations have a deep influence upon a person’s willingness to look for opportunity, what they see, and how they pursue them [24].

Many new technology innovations are pushed into the market and in some cases, products and services go on to be very successful, i.e., iPad, iPhone, personal computer, automobile, airplane, and steam engine[25]. Any new technology will have a number of potential applications[26], and the inventor/entrepreneur or firm must decide which area is most lucrative one to focus upon. Any new technologies must solve existing problems effectively and efficiently, and be able to provide consumers with benefits. Every invented device, process, or service requires an innovation period where the invention is matched with opportunity, as the new technology is not an opportunity within itself. This requires a clear understanding of what customers are looking for and why they buy. Finding this out may be a “hit and miss” process where mistakes can be very costly and punished very quickly[27].

Consequently, the pursuit of new knowledge and technology is an endogenous phenomenon where technology must be matched to an idea. Thus an opportunity is created by an entrepreneur or team working with him or her[28]. Opportunities are generated through the quest for new knowledge. Opportunities may then be more prevalent in industries where more new knowledge is generated, i.e., biotechnology and ICT, etc, than prevailing in low technology industries [29]. In this context some opportunities can only emerge when the technology exists and has been applied as an idea to something. Thus, opportunity streams into the environment through ideas to apply new technologies when they exist.

Finally it is perhaps worthwhile to distinguish opportunity from speculation. Because the future is never certain, activity that takes place overtime is to some degree speculative. Opportunities are based on the belief that value can be created which will yield future profits and any uncertainties are manageable if resources are deployed effectively within the control of the entrepreneur. The profits resulting from entrepreneurial opportunity exploitation are derived from a deliberate set of actions and the successful creation of value. Speculation however relates to a bet on an outcome, where a person may think that prices will either rise or fall in the future and base their actions upon this belief or speculation. If they believe prices will rise in the future, they will buy, if they believe prices will fall in the future, they will defer or postpone buying. This can be applied to anything that can be bought or sold and speculation tends to be successful in markets that are on a continual rise. The availability of credit tends to fan speculation. Speculators risk their capital in the expectation that the price in the market will shift to favour their position. Speculation unlike opportunity exploitation is usually paper based that does not create any new value and outcomes are usually outside the control of the investor unless large sums of capital are utilized and has influence over market price levels. In these cases, speculation becomes distortive and profits are made through the distortion of the market. Speculation is usually motivated by the desire for quick gains and relies on the exogenous forces of demand, supply (market volatility) and speculation to achieve monetary gains, rather than acts of creation.

The Forms of Opportunity

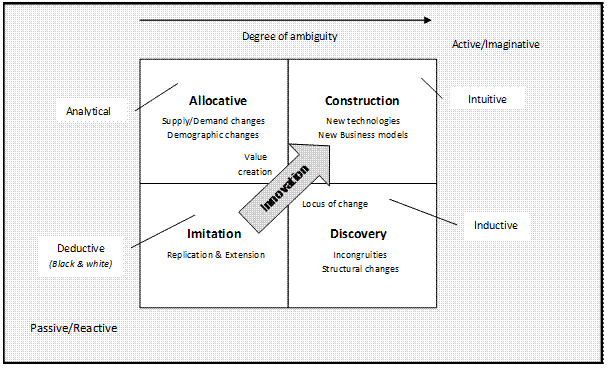

Opportunities manifest themselves in different ways and can be categorized accordingly. One of the simplest ways of mapping forms of opportunities is by the locus of change they manifest into the environment. Less innovative forms of opportunity tend to be passive/reactive imitation or rent seeking activities, while active/imaginative forms of opportunities tend to require a proactive intervention into the environment where an entrepreneur seeks to change things. Allocative opportunities involve finding new market space through passive analysis of demand and supply and demographics, while the other sector discovery opportunities involve more active entry into the market place with products aimed at developing new market space believed to exist where incongruities and structural change may be taking place. Each form of opportunity is likely but not exclusively associated with a style of thinking as depicted in figure 1.

Figure 1. The forms of opportunity.

Imitation based Opportunities

Imitation is the most basic form of opportunity. The imitative continuum requires little innovation and there is little value creation. Entrepreneurs see effective business models and utilize the ideas contained within them for their own benefit. There are usually few changes made to any of these observed business models and they are usually adopted in whole with minimal modification. The key for the individual is to select a suitable geographical location or customer group to target and focus upon. The thinking style and narrative would tend to be some form of arbitrary reasoning in the manner of “people need to buy groceries and there is room for a grocery store in this area”, “people need to buy a cup of coffee, sandwich, and newspaper on their way to work, outside this railway station”, and “The residents in this apartment building could do with the convenience of a washing and ironing service”. Imitation is reactive upon what a person sees is successful for others, probably with the prime goal of earning a living. This does not differ too much at the corporate level where most companies tend to imitate their competitors, as imitation is perhaps perceived to be a less risky option. Imitation opportunities are usually most effective in safe unambiguous environments, although also highly successful against first movers in technology based high growth markets like what is occurring to the iPad.

It is not too difficult to quantify the size of the opportunity and the key issues are how much market share a firm can obtain and how much will it cost to obtain it. The simplest form of imitation is straight out copying, spanning out into the extension of an idea, and duplication in other markets.

Allocative based Opportunities

Allocative opportunities occur when there are mismatches in supply and demand, resources are scarce in certain areas, an individual or firm has a resource monopoly, or demographic changes require specific products and services to fulfil emerging needs and wants. Allocative opportunities primarily occur out of market imperfections or changing demographics which can be identified on the most part through scanning and analysis of the competitive environment. This analysis may show where goods and services are absent, prices are inefficient, and where supply channels and value chains are not effective. Allocative opportunities represent the demand and supply issues in classical economic theory.

Allocative opportunities can be identified through market observation and information. Once identified allocative opportunities can be easily seen, i.e., the shortage of particular goods and services in the market, or an aging population or baby boom requiring specific sectional goods and services. The potential of allocative opportunities are greatly enhanced for firms that already serve these markets and have established supply chains and channels of distribution with strong sales networks. The key to recognising opportunities is through environmental scanning. A powerful source of ideas is through observing similar markets in other countries for new products that have not reached the entrepreneur’s market yet, especially in developing markets. There is more innovation and value creation in developing allocative opportunities than with imitation opportunities, but these types of opportunities still remain within a passive/reactive strategic approach. Like imitation, allocative opportunity values are not too difficult to forecast in most cases.

Discovery based Opportunities

Changes in technology, consumer preferences, regulation, and economic conditions most often lead to opportunity gaps within the competitive environment. Opportunities are derived from the attributes of the industry independent of an entrepreneur’s action. These opportunities await discovery by an alert individual who may or may not decide to exploit them[30]. If an entrepreneur can understand the attributes and structure of an industry, then he or she will be able to anticipate the type of opportunities available within the industry. These discoveries may require the recombination of old and new knowledge in novel ways to find viable opportunities [31]. However specific industry knowledge is very important and an individual through industry experience may be able to see industry opportunities that people without specific industry knowledge cannot see [32]. In addition, people with specific industry experience may discover opportunities without any systematic search[33].

The use of discovery is suitable under conditions of risk and uncertainty where pre-existing information exists about the nature of opportunities in question. The discovery process is also good where firm and industry structure requires change like the need to create economies of scale of lower a firm/industry cost base[34]. The value of the opportunity is extremely difficult to forecast with discovery opportunities until sales actually occur within the market. Inductive reasoning is often used in the discovery process although rational, analytical, and intuitive thinking can also play an important role in the development of the opportunity.

Construction based Opportunities

Some opportunities do not exist until they are constructed by someone[35]. Opportunity construction[36] tends to be unrelated to present information and created through an emergent process of trial and error within the competitive environment[37]. The entrepreneur through experience and interaction with the environment crafts a new opportunity [38]. The entrepreneur does not become aware of the opportunity by reconfiguring information and knowledge in new ways, rather new knowledge is built up through action creating new information from closely observing the results of the intervention within the competitive environment and changing the nature of action according to the results gained[39]. The final result from an entrepreneur’s efforts will not be known at the beginning of the opportunity construction process as the future outcome may be totally different to what was originally conceived and irrelevant to present information [40]. A viable opportunity is the eventual result of these actions, resulting from feedback and further action [41].

Opportunity construction is a path dependent process where an entrepreneur learns what works and what doesn’t work as the process of developing a venture progresses (Arthur 1989). The entrepreneur may not immediately discover the most lucrative aspect of the opportunity first off, he or she may enter into a business which has been identified as part of an opportunity and as experience accumulates, learning occurs where the firm rolls into the full potential of the opportunity by modifying focus, strategies, target customers, etc. For example an entrepreneur may establish a boutique handmade chocolate business but find market sales don’t work as well as hi-teas, so the entrepreneur changes focus and strategy away from the product towards running events. The more novel the opportunity that is ultimately constructed through this process, the more learning and new information is required through experimentation [42]. For innovative new products and services customer information is of little use [43]. It is extremely difficult to forecast the value of construction opportunities as it takes time for the entrepreneur to develop a stable income earning business model.

Construction opportunities are an exploratory process where learning through trial and error is a valuable part of developing the opportunity[44]. Failure to learn from action will almost certainly result in failure. Successful opportunity construction may involve many adjustments to action through reinterpreting the results which may require starting all over again or abandoning the idea all together [45]. As the emergence process continues entrepreneurs may be forced to redefine their customers, markets, or even industry they are operating within, technologies and question the original assumptions about the opportunities they are pursuing[46].

Prior industry knowledge may hinder learning[47] as the individual maybe locked into pre-existing ideas and knowledge. By breaking out of this industry ‘conformity’, new ideas, processes, and business models can be developed and introduced into an industry[48].

Opportunity construction primarily relies on intuitive thinking to tap a person’s creativity and imagination. The process of effectuation discussed in chapter three is very common where an enterprise is built upon what is available rather than deciding what is needed before start-up. This approach results in incremental ‘step by step’ growth where resources are acquired as needed, i.e., a new airline purchases aircraft as it is able to open and develop new routes. These types of opportunity are socially constructed [49], within the confines of the culture the entrepreneur is immersed within. Opportunity construction is powerful where little knowledge is available, especially where new technologies or new business models are concerned. Under conditions of uncertainty, learning is probably more useful than planning[50]. Opportunities in this form have fewer precedents to learn from other forms of opportunity and entrepreneurs will develop their own knowledge structures to give the information they generate form and meaning[51]. Constructed opportunities are usually the most disruptive to the competitive environment.

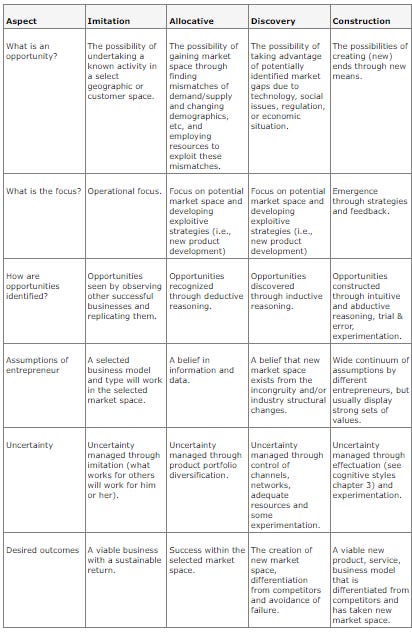

All of these forms of opportunities exist in the real world [52]. Which form of opportunity is manifested to the entrepreneur will depend upon the information available and level of ambiguity, and it may not be uncommon for entrepreneurs to switch from using one form to another in developing the opportunities they exploit[53]. As time goes on more information may exist where the discovery mode may become the most apt aid in opportunity development. A comparison between the four forms of opportunity is shown in Table 1.

Table 1. A comparison of the four forms of opportunity.

Large firms in markets where the level of ambiguity is low will tend to rely on rational and analytical approaches to opportunity recognition, often constrained by the formal strategic planning and management processes they have in-place[54]. A major part of management literature today focuses upon assisting corporations shed themselves of their rigidities and tunnel vision to become more innovative and entrepreneurial. To many SMEs, opportunity is the only strategy that the entrepreneur has. Opportunity is firmly implanted within the entrepreneur’s mind and vision, and all efforts and initiatives focus upon exploiting it and learning through doing, trial and error, making mistakes, feedback from peers and customers, etc, copying others, solving problems, and general experimentation[55].

Originally published in Orbus, July 2013

You can subscribe for free emails of future articles here:

Notes and References

[1] Sarasvathy, S.D. (2002). Causation and Effectuation: Toward a theoretical shift from economic inevitability to entrepreneurial contingency, Academy of Management Review, Vol. 26, No. 2, pp. 243-288.

[2] Shane, S. (2003). A General Theory of Entrepreneurship, Northampton, MA. Edward Elgar Publishing.

[3] Kirzner, I. (1973). Competition and Entrepreneurship, Chicago, University of Chicago Press.

[4] Muzyka, D. (1997). Spotting the market opportunity, In: Birley, S. & Muzyka, D. (Eds.), Mastering Enterprise, London, Financial Times, Pitman Publishing, pp. 28-31.

[5] Carland, J.A., Carland, J. & Stewart, W.H. (1996). Seeing what’s not there: The enigma of entrepreneurship, Journal of Small Business Strategy, Vol. 7, No. 1, pp, 1-20.

[6] Gestalt in this situation is the formation of something whole through insight, intuition, and other forms of mental construction

[7] Griffin, A. (1997). The Drivers of NPD Success: The PDMA Report, Chicago, Product Development & Management Association

[8] Foster, R., N., (2000), ‘Managing Technological Innovation for the Next 25 Years’, Research-Technology Management, 43, 1., Jan/Feb., P. 20.

[9] Kearney, R. (1998). Poetics of Imagining: Modern to Postmodern, New York, Fordham University Press, P. 3.

[10] Wiener, N. (1993). Invention: The Care and Feeding of Ideas, Cambridge, MA, MIT Press, P. 7..

[11] Levitt, T. (1986), The Marketing Imagination, New Expanded Edition, New York, Free Press, P. 127.

[12] Brown, S. & Patterson, A. (2000). Figments for sale: marketing, imagination and the artistic imperative, In: Brown, S. & Patterson, A. (Eds.), Imagining Marketing: Art, Aesthetics and the Avant-Garde, London, Routledge, P. 7.

[13] Bhide, A. (1999). How Entrepreneurs Craft Strategies that Work, Boston, Harvard Business School Press.

[14] Cooper, R.G. (2001). Winning at New Products: Accelerating the Process from Idea to Launch, 3rdEdition, New York, basic Books, P. 95.

[15] Stevenson, H.H. & Jarillo, J.C. (1990). A Paradigm of Entrepreneurship: Entrepreneurial Management, Strategic management Journal, Vol. 11, Special issue: Corporate Entrepreneurship, pp. 17-27.

[16] Wickham, P.A. (2006). Strategic Entrepreneurship 4thEdition, New York, Prentice Hall.

[17] Schumpeter, J. (1934). Capitalism, Socialism, and Democracy, New York, Harper & Row, Casson, M. (1982). The Entrepreneur, Totowa, NJ, Barnes & Noble Books.

[18] Shane, S. (2003). “A General Theory of Entrepreneurship”.

[19] Stevenson, H. H. & Gumpert (1985). The heart of entrepreneurship, Harvard Business Review, March-April, pp. 85-94.

[20] Venkataraman, S. (1997). The distinctive domain of entrepreneurship research: an editor’s perspective, In: Katz, J. & Brockhaus, R. (Eds.), Advances in entrepreneurship, firm emergence and growth, Vol. 3, Greenwich, CT, JAI Press, pp. 119-138.

[21] Von Hippel, E. (1994). “Sticky Information” and the locus of problem solving: Implications for innovation, Management Science, Vol. 40, No. 4, pp. 429-439.

[22] Wildeman, R.E., Hofstede, G., Wennekers, A.R.M. (1999). Culture’s role in entrepreneurship: Self-employment out of dissatisfaction, Rotterdam, Rotterdam Institute for Business Economic Studies.

[23] Meredith, G.G., Nelson, R.E., & Neck, P.A. (1982). The Practice of Entrepreneurship, Geneva, International Labour Office.

[24] Reynolds, P., Bygrave, W., Aoutio, E. (2004). Global Entrepreneurship Monitor (GEM) 2003 Global Report, MA., Babson College,

[25] This is in contrast to a product or service being designed around unsatisfied consumer needs and wants.

[26] The steam engine could be utilized as a factory power plant, an automobile power plant, or locomotive steam engine, etc. However early steam engine inventors saw the biggest potential of the steam engine for mine pumps and factory power plants to drive machinery.

[27] Wickham, P.A. (2006). Strategic Entrepreneurship 4thEdition, New York, Prentice Hall, P. 189.

[28] Griliches, Z. (1979). Issues in assessing the contribution of R&D to productivity growth, Bell Journal of Economics, Vol. 10, pp. 92-116.

[29] Cohen, W.M. & Klepper, S. (1991). Firm size verses diversity in the achievement of technological advance, In: Acs, Z.J. & Audretsch, D.B. (Eds.), Innovation and Technological Change: An International Comparison, Ann Arbor, University of Michigan Press, pp. 183-203, Cohen, W.M. & Klepper, S. (1992). The tradeoff between firm size and diversity in the pursuit of technological progress, Small Business Economics, Vol. 4, No. 1, pp. 1-14.

[30] Kirzner, I. (1973). ‘Competition and Entrepreneurship’, P. 7.

[31] Shane, S. (2003). “A General Theory of Entrepreneurship”

[32] Casson, M. (1982). “The Entrepreneur”.

[33] Barney, J.B. (1986). Strategic factor markets: expectations, luck, and business strategy, Management Science, Vol. 32, No. 10, pp. 1231-1241.

[34] Porter, M.E. (1990). The Competitive Advantage of Nations, New York, Free Press.

[35] Baker, T. & Nelson, R. (2005). Creating something from nothing: Resource construction through entrepreneurial bricolage, Administrative Science Quarterly, Vol. 50, pp. 329-366, Gartner, W.B. (1985). A conceptual framework for describing the phenomenon of new venture creation, Academy of Management Review, Vol. 10, pp. 696-706., Weick, K.E. (1979). The Social Psychology of Organizing, Reading, MA, Addison-Wesley.

[36] Often referred to as creation theory.

[37] Mintzberg, H. & Waters, J.A. (1985). Of Strategies, Deliberate and Emergent, Strategic Management Journal, Vol. 6, No. 3, pp. 257-272.

[38] Ardichvili, A., Cardozo, R., & Ray, S. (2003). A theory of entrepreneurial opportunity identification and development, Journal of Business Venturing, Vol. 18, pp. 105-123., Chell, E. (2000). Towards researching the “opportunistic entrepreneur”: a social construction approach and research agenda, European Journal of Work and Organizational Psychology, Vol. 9, No. 1, pp. 63-80, Kruger, N. (2000). The cognitive infrastructure of opportunity emergence, Entrepreneurship, Theory, & Practice, Vol. 24, No. 3, pp. 5-23.

[39] Choi, Y.B. (1993). Paradigms and Conventions: Uncertainty, Decision Making and Entrepreneurship, Ann Arbor, University of Michigan Press.

[40] Sine, W.D., Haverman, H.A., & Tolbert, P.S. (2005). Risky Business? Entrepreneurship in the new independent power sector, Administrative Science Quarterly, Vol. 50, pp. 200-232.

[41] Weick, K.E. (1979). “The Social Psychology of Organizing”

[42] Galbraith, J.R. (1977). Designing Complex Organizations, Reading, MA, Addison-Wesley, Schoonhoven, C.B., Eisenhardt, K.M. & Lyman, K. (1990). Speeding products to market: Waiting time to first product introduction in new firms, Administrative Science Quarterly, Vol. 35, No. 1, pp. 177-207.

[43] Spinelli, S., Neck, H.M., & Timmons, J.A. (2007). The Timmons Model of the Entrepreneurial Process, In: Zacharakis, A. & Spinelli, S., (Eds.). Entrepreneurship: The Engine of Growth, Volume 2, Process, Westport CN, Praeger Perspectives, P. 6.

[44] Rindova, V. & Kotha, S. (2001). Continuous morphing: Competing through dynamic capabilities, form, and function, Academy of Management Journal, Vol. 44, pp. 1263-1280.

[45] Cyert, R.M. & March, J.G. (1963). A Behavioral Theory of the Firm, Englewood Cliffs, NJ. Prentice-Hall, March, J.G. & Simon, H.A. (1958), Organizations, New York, John Wiley, Mosakowski, E. (1997). Strategy Making Under Causal Ambiguity: Conceptual issues and Empirical Evidence, Organizational Science, Vol. 8, No. 4, pp. 414-442.

[46] Bhide, A. (1992). Bootstrap Finance: The art of start-ups, Harvard Business Review, Vol. 70, No. 6, pp. 109-117, Bhide, A. (1999). How Entrepreneurs Craft Strategies that Work, Boston, Harvard Business School Press, Christensen, C.M., Anthony, S.D., & Roth, E.A. (2004). Seeing What’s Next, Boston, Harvard Business School Press.

[47] March, J.G. (1991). Exploration and exploitation in organizational learning, Organizational Science, Vol. 2, No. 1, pp. 71-87., Sine, W.D., Haverman, H.A., & Tolbert, P.S. (2005). Risky Business? Entrepreneurship in the new independent power sector, Administrative Science Quarterly, Vol. 50, pp. 200-232, Weick, K.E. (1979). “The Social Psychology of Organizing”.

[48] Aldrich, H.E. & Ruef, M. (2006). Organizations Evolving, 2ndEdition, Thousand Oaks, Sage.

[49] Berger, P.L. & Luckmann, T. (1967). The Social Construction of reality: A Treatise in the Sociology of Knowledge, New York, Anchor Books Doubleday and Company, Inc.

[50] Argote, L. (1999). Organizational Learning: Creating, Retaining and transferring Knowledge, Norewell, Kluwer Academic Publishers.

[51] Walsh, J.P. (1995). Managerial and Organizational cognition: Notes from a trip down memory lane, Organization Science, Vol. 6, No. 3, pp. 280-321.

[52] Daft, R. L. & Weick, K.E. (1984). Toward a model of organizations as interpretation systems, Academy of Management Review, Vol. 9, No. 2, pp. 284-295.

[53] Hannan, M.T. & Freeman, J. (1977). The population ecology of organizations, American Journal of Sociology, Vol. 82, pp. 50-73, Rindova, V. & Kotha, S. (2001). Continuous morphing: Competing through dynamic capabilities, form, and function, Academy of Management Journal, Vol. 44, pp. 1263-1280.

[54] Fredrickson, J.W. (1983). Strategic processes research: Questions and Recommendations, Academy of Management Review, Vol. 8, pp. 565-575, Fredrickson, J.W. (1986). The strategic decision process and organizational structure, Academy of Management Review, Vol. 11, No. 2, pp. 280-297, Mintzberg, H. (1994). The rise and fall of strategic planning, New York, Free Press.

[55] Gibb, A.A.(1997). Small Firm’ Training and Competitiveness. Building Upon Small Business as a learning Organization, International Small Business Journal, Vol. 15, No. 3, pp. 13-29.