Smoke & Mirrors: The illusions of Islamic banking

Islamic banking today is just a half measure

Islamic banking is growing exponentially throughout the world. This is no different in Malaysia, where Islamic banking and finance is a USD 300 billion market, growing around 14 percent per annum. According to Bank Negara Malaysia, Islamic banking assets reached USD 254 billion by 2020, where today Islamic banking represents 40 percent of the total banking sector.

Today there are 11 local, and 5 foreign Islamic banks and Takaful in Malaysia. Takaful represents around 30 percent of the Islamic banking sector.

The three basic principles of Islamic banking are the prohibition of riba, or interest and/or excess profiteering, the elimination of gharar or uncertainty, and the banning of maisar, or gambling. Islamic banking must comply with Shariah law under the concept of the Tawhid, the umbrella of the Islamic theology.

Islamic banking is a human innovation, and as a consequence, is not a divine creation. It’s based upon human interpretations of the Al Quran and Hadiths, and thus has faults and imperfections. So, mistakes are possible.

The Malaysian Islamic banking sector has undertaken a lot of experimentation and innovation since Islamic banking begun in 1983. The first Islamic banks were offshoots or adjuncts of the major local conventional banks. Islamic banking products were just extra products flowing through their existing systems and infrastructure. Thus, Malaysia became a dual banking system. A major issue is just how integrated are Islamic products are with conventional banking.

One of the major issues within Islamic banks is riba. Interest is a time value calculation made upon the renting of money to a second party. The second party is obligated to pay back the principal and a charge for the use of the money. These charges on money from Islamic banks very closely reflect rates charged by conventional banks. The cost of money from Islamic banks on face value appears to be just a reframing of interest.

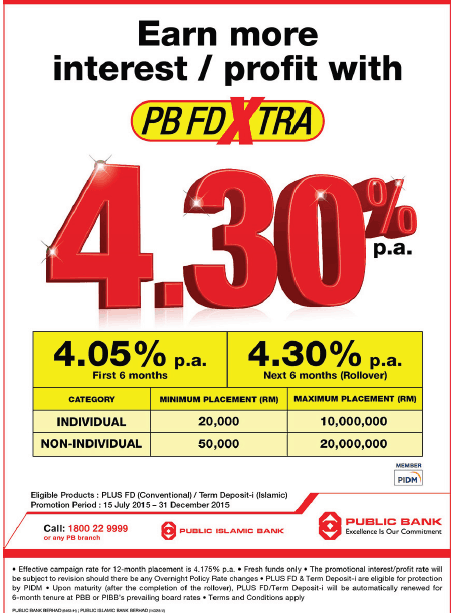

Islamic banks in Malaysia even advertise interest rates on the deposit accounts they offer their customers.

Term deposit return rates as advertised in percentage terms in Islamic banks. This very closely resembles an interest rate provided by conventional banks. A percentage charged or paid over time on a sum of money is an interest rate.

The biggest theological issue facing Islamic banks in the present economy, is that it is operated on debt and return as a means to make a profit. The profit made upon loans is the way economies expand the money supply. Thus, modern economies expand upon riba.

Islamic banks operate with a form of money that is built upon riba

A number of verses within the Al Quran advocate the use of intrinsic forms of currencies like gold, silver, and commodities. These verses include Imran, 3:75, 3:91, and 3:14, Yusuf, 12:20, Al-Tauba, 9:34, Zukhruf, 43: 71, 43:53, 43:33-5, Al-Nisa, 4:20, Al- Insan 76: 21, Al-Fatir, 35:33, Al-Hajj, 22:23, Al-Kahf, 18:31, and Al-Isra, 17:93.

A true Islamic monetary system should be based upon the gold Dinar, and silver Dirham. This is the true currency of an Islamic monetary system. The Malaysian Islamic banking system is operating with fiqh money, that is not redeemable.

An important Hadith says “Gold for gold, silver for silver, wheat for wheat, barley for barley, dates for dates, and salt for salt. (When a transaction is) like for like, payment being made on the spot, then if anyone gives more, or asks for more, he has dealt in riba. The receiver and the giver being equally guilty (Muslim).

The Malaysian government forbids the use of the Dinar and Dirham as a form of legal tender in Malaysia

This implies money should have an intrinsic value, and as a consequence, a real store of value.

With the advent of central banks now in the process of developing digital currencies, a Hadith provides Muslims with a clear warning of what is going to happen.

“A time is certainly coming over mankind in which there will be nothing (left) that will be of use (or benefit), save a Dinar and a Dirham.” (Abu Bakr).

Subscribe Below:

In 2006, I went before Parliament, on February 13th, to REGISTER a similar cultural protest about the "smoke and mirrors I had observed from 32 years in the Public Services!" To date, I have not received any formal reply! KJJ